Practical Financial Advice: Smart Investing & Money Management Strategies

Welcome to your financial freedom journey, where we turn complex numbers into actionable steps! Managing money isn’t just about math; it’s truly about mastering your behavior and psychology. You need a budgeting blueprint that works for your unique lifestyle rather than against it. The 50/30/20 rule is a fantastic place to start: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It’s vital to track every dollar so you can see exactly where your financial leaks are occurring. Think of every dollar you earn as an employee that needs a specific job to do. Without a clear plan, your hard-earned cash will simply disappear into the void of impulse buys.

- Needs: Rent, utilities, and essential groceries.

- Wants: Dining out, subscriptions, and hobbies.

- Savings: Emergency funds and long-term investments.

Creating a sustainable spending plan helps you say ‘yes’ to the things that truly matter. Don’t be too hard on yourself if you slip up occasionally on your journey. Consistency over perfection is the ultimate secret to long-term success in money management. Let’s dive deep into how you can transform your relationship with money starting right now.

Before you can sprint toward wealth, you must handle your historical baggage, specifically high-interest debt. Credit card debt is a notorious wealth killer that grows much faster than most traditional investments ever will. You should categorize all your debts and tackle the ones with the highest APR first, a strategy known as the Avalanche Method. Alternatively, the Snowball Method focuses on paying off the smallest balances first to build vital psychological momentum. While you’re aggressively doing this, building an emergency fund is non-negotiable for your long-term peace of mind. Aim for 3 to 6 months of living expenses tucked away in a high-yield savings account. This acts as a sturdy financial buffer against life’s unexpected curveballs like car repairs or sudden medical bills.

- Emergency Fund: Your essential safety net for rainy days.

- Debt Snowball: Achieving small wins for big motivation.

- Debt Avalanche: Mathematical efficiency for maximum interest savings.

Once your high-interest debt is finally gone, you’ll feel a massive weight lift off your shoulders. This transition allows you to move from defensive financial tactics to offensive wealth-building moves. Taking control of your liabilities is the first step to becoming a truly savvy and confident investor.

Now, let’s talk about the engine of wealth: Smart Investing. You don’t need to be a Wall Street wizard or have a finance degree to see great returns over time. In fact, most experts recommend low-cost index funds because they offer instant diversification across the entire stock market. Diversification is your best friend because it lowers your risk profile significantly while you sleep. Instead of trying to pick the next ‘hot’ individual stock, focus on capturing the growth of the global economy as a whole. Time in the market is always significantly better than trying to time the market’s peaks and valleys. Even small amounts invested today can grow into a substantial nest egg thanks to the magic of compounding interest. Don’t let short-term market volatility scare you into selling your assets when prices are temporarily low. Stay the course, keep your management fees low, and watch your portfolio flourish over the decades. Investing is a marathon, not a sprint, so patience is truly a virtue in this game. Research consistently shows that passive investing often outperforms active trading over the long haul. Focus on what you can actually control, like your savings rate and your investment costs.

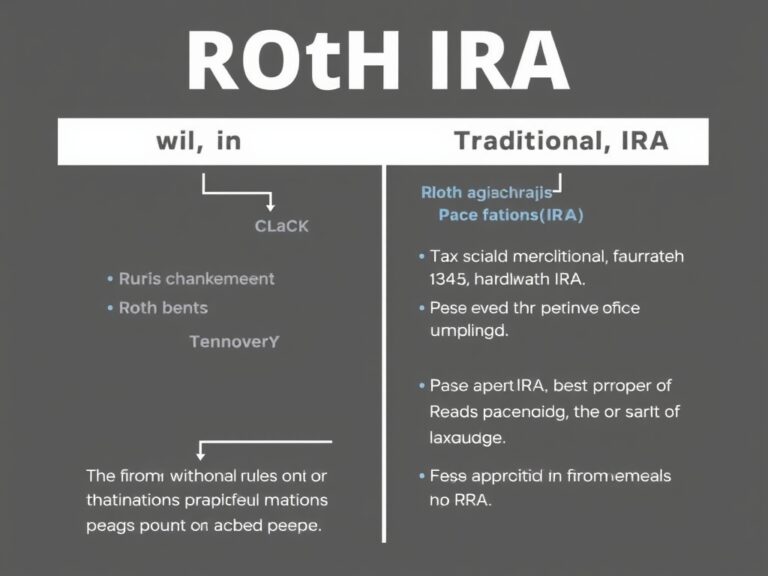

Retirement planning might seem like it’s far away, but it’s the most critical financial goal you’ll ever work toward. You should always maximize your employer’s 401(k) match if they offer one because it’s essentially free money for your future. Beyond that, consider opening a Roth IRA for its incredible tax-free growth benefits during your golden years. Understanding the nuances between pre-tax and post-tax contributions can save you thousands of dollars in the long run. It’s also vital to rebalance your portfolio annually to ensure your asset allocation still matches your risk tolerance. As you get closer to your target retirement date, you might want to shift toward more conservative investments to protect your capital. Don’t forget to account for inflation when calculating how much you’ll actually need to live comfortably in the future. Having a clear target number makes the long journey much more tangible and achievable for the average person. Consult with a certified financial professional if you’re feeling overwhelmed by the technicalities of estate planning. Your future self will thank you for the diligence and discipline you’re showing today. Retirement is not an age; it is a financial status you achieve through careful and persistent planning. Make sure you are also looking into health savings accounts as a secondary, tax-advantaged investment vehicle.

Finally, the absolute key to staying wealthy is continuous learning and automation. Automate your monthly transfers so that your savings and investments happen before you even see the money in your checking account. This simple trick removes the temptation to spend and ensures your financial goals are met every single month without fail. Keep your lifestyle inflation in check even as your income grows over the span of your career. Just because you get a significant raise doesn’t mean you immediately need a more expensive car or a bigger house. Instead, use those extra funds to accelerate your path to total financial independence. Stay curious about new financial strategies, but always remain skeptical of ‘get-rich-quick’ schemes that sound too good to be true. Surround yourself with a community of like-minded individuals who value financial literacy and open discussion.

- Automation: Set it and forget it for consistent, hands-off growth.

- Lifestyle Creep: The silent enemy that prevents true wealth building.

- Financial Education: The best investment you can ever make is in yourself.

Success is built on small, daily habits that compound into massive results over several decades. You now have the tools and the knowledge, so it’s time to take action and secure your financial legacy. Remember, the best time to start was yesterday, but the second best time is today.