Practical Financial Advice: Smart Investing & Money Management Strategies

Setting Your Financial Foundation with Smart Budgeting

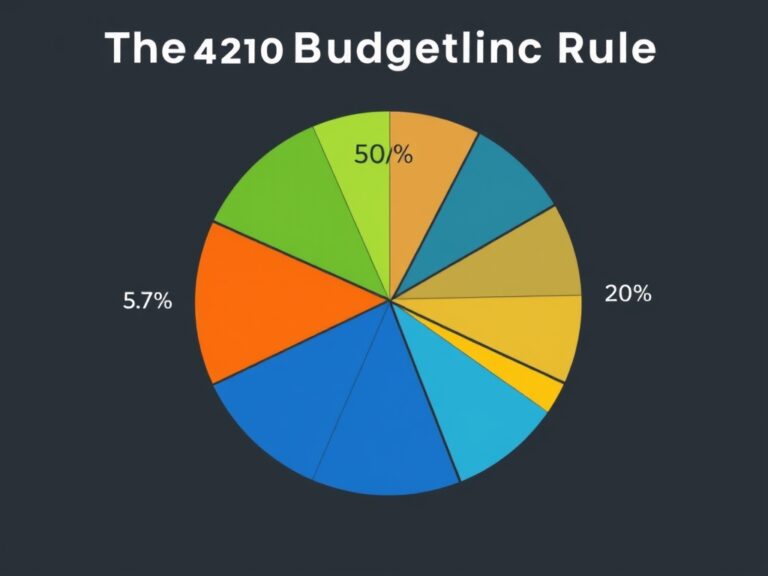

Hello there! Taking control of your finances might feel overwhelming at first, but I promise you that smart money management is a skill anyone can master with the right approach and a bit of discipline. The first step in any successful financial journey is establishing a solid foundation, which starts with understanding exactly where your money goes each month. One of the most effective tools for this is the 50/30/20 budgeting rule, a simple yet powerful framework that categorizes your spending into three main buckets.

- 50% for Needs: This covers your essentials like rent, utilities, and groceries.

- 30% for Wants: This allows for lifestyle choices like dining out, hobbies, and streaming services.

- 20% for Savings: This is dedicated to debt repayment, emergency funds, and investing.

By following this ratio, you ensure that your essential costs are covered while still leaving room for personal enjoyment and future growth. Many people find that tracking their expenses using an app or a spreadsheet reveals hidden ‘leaks’ in their budget that they never noticed before. It’s not about restricting yourself to a life of boredom; it’s about making sure your spending aligns with your long-term values. Once you have a clear picture of your cash flow, you gain the confidence to make informed decisions rather than reactive ones. Remember, every dollar has a job, and your job is to tell it where to go so it doesn’t just disappear. Start by looking at your last three months of bank statements to see how your current habits stack up against the 50/30/20 ideal. This clarity is the bedrock upon which you will build your future wealth and financial independence.

Crushing Debt and Building Your Safety Net

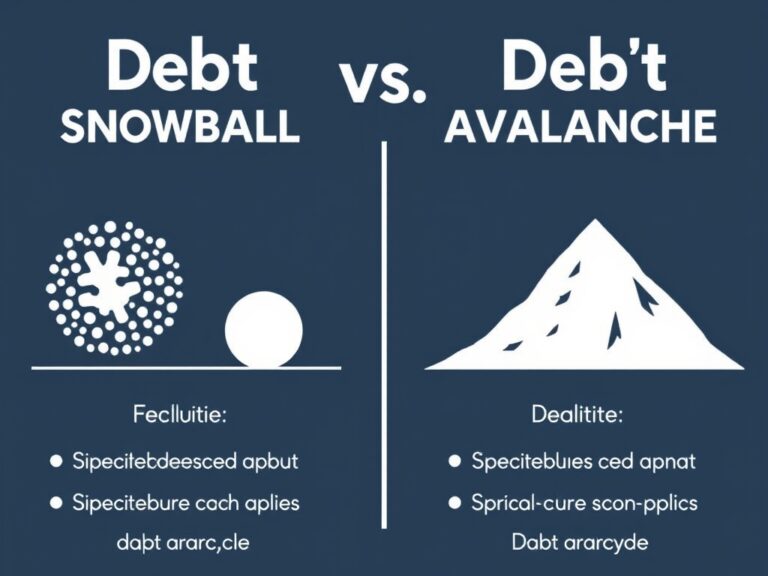

Once your budget is in place, the next critical step is to tackle high-interest debt and build a protective barrier between you and life’s unexpected surprises. Carrying credit card debt is like trying to run a marathon with weights tied to your ankles because the interest rates often exceed the returns you could earn by investing. High-interest debt should be treated as a financial emergency, and you might consider strategies like the Debt Avalanche method or the Debt Snowball method to gain momentum.

- Debt Avalanche: Focus on paying off the balance with the highest interest rate first to save money over time.

- Debt Snowball: Pay off the smallest balances first to gain psychological wins and motivation.

While you are paying down debt, you must simultaneously work on an emergency fund that covers three to six months of your essential living expenses. Having this cash cushion in a high-yield savings account ensures that a car repair or medical bill doesn’t force you back into high-interest debt. It provides a sense of psychological security that is truly priceless when market volatility or job changes occur. Think of this fund as your ‘sleep well at night’ insurance policy that protects your long-term investments. Without this safety net, even the best investment strategy can crumble when a short-term crisis hits. By prioritizing liquidity and debt reduction today, you are effectively buying back your freedom from creditors for the future. You deserve the peace of mind that comes with knowing you can handle whatever life throws your way.

Investing for the Long Haul: The Power of Compounding

Now that your foundation is secure, let’s talk about smart investing strategies that can help your wealth grow exponentially over time through the miracle of compound interest. You don’t need to be a Wall Street expert to be a successful investor; in fact, some of the most successful individuals use a simple, hands-off approach. Diversification is your best friend here, as it involves spreading your money across different asset classes like stocks, bonds, and real estate to reduce overall risk.

- Index Funds: These allow you to own a small piece of the entire stock market at a very low cost.

- ETFs: Exchange-Traded Funds offer flexibility and can track specific sectors or broad indices.

- Asset Allocation: This is the process of balancing your portfolio based on your unique age and risk tolerance.

Instead of trying to ‘time the market’ or pick the next hot stock, focus on ‘time in the market,’ which has historically proven to be a much more reliable path to wealth. When you invest consistently, even during market downturns, you benefit from Dollar Cost Averaging, which lowers your average purchase price over time. It’s important to keep your investment fees low, as high management fees can eat away a significant portion of your gains over several decades. Investing is a marathon, not a sprint, and patience is often rewarded more than frantic activity or chasing trends. By starting as early as possible and staying consistent, you allow the power of compounding to do the heavy lifting for your bank account. Your future self will thank you for the seeds you are planting today.

Maximizing Tax-Advantaged Growth and Retirement

To truly optimize your money management strategies, you must take full advantage of tax-advantaged retirement accounts and any benefits your employer might offer. If your company offers a 401(k) match, that is essentially a 100% return on your money and should be your absolute top priority in your investment hierarchy. Beyond the employer match, consider contributing to a Roth IRA or a Traditional IRA, depending on your current income level and your expectations for future tax rates.

- 401(k): Often provides a tax deduction today and allows your money to grow tax-deferred until retirement.

- Roth IRA: Contributions are made after-tax, but your withdrawals in retirement are completely tax-free.

- HSA: A Health Savings Account offers a triple tax advantage if used for qualified medical expenses.

Understanding the nuances of the tax code allows you to keep more of what you earn, which significantly accelerates your journey to financial independence. Many people overlook the impact of taxes on their long-term returns, but choosing the right account type can mean the difference of hundreds of thousands of dollars later in life. It’s also wise to automate your contributions so that your ‘future self’ gets paid before you even have a chance to spend that money. This ‘pay yourself first’ mentality ensures that your retirement goals aren’t left to whatever is left over at the end of the month. By structuring your investments efficiently, you are building a robust financial engine that works for you even while you sleep.

Mastering Your Money Mindset and Long-Term Success

Finally, the key to long-term success in practical financial advice is maintaining a disciplined mindset and periodically reviewing your strategy to ensure it still aligns with your life goals. Markets will fluctuate, and headlines will often scream about impending doom, but a successful investor stays the course and ignores the short-term noise. Rebalancing your portfolio once a year is a great way to sell high and buy low without even thinking about it, as it brings your asset allocation back to its original target.

- Quarterly Reviews: Check your budget every few months to adjust for life changes or new goals.

- Annual Rebalancing: Reset your investment percentages to maintain your desired risk level.

- Continuous Learning: Stay curious about new financial tools, but stick to the fundamentals that work.

It is also vital to continue educating yourself, as the financial world is always evolving with new regulations and opportunities. Don’t be afraid to seek professional advice from a fiduciary financial advisor if your situation becomes complex, as they are legally obligated to act in your best interest. Ultimately, money is just a tool to help you live the life you want, so make sure your financial plan reflects your personal values and aspirations. Stay focused on the big picture, celebrate your small wins along the way, and don’t get discouraged by temporary setbacks or market dips. With persistence and these smart strategies, you are well on your way to achieving lasting financial peace and prosperity for years to come.