Practical Financial Advice: Smart Investing & Money Management Tips

### Step 1: Mastering Your Cash Flow with Smart Budgeting

Let’s dive into the world of smart money management by first mastering your cash flow, which is the heartbeat of your financial health. Managing money isn’t just about spreadsheets; it’s about aligning your daily spending with your long-term life goals and values. Most people struggle because they don’t truly know where their hard-earned money goes every single month. Use the 50/30/20 rule as a benchmark to simplify your life:

- 50% for Needs: covering essentials like rent, groceries, and utilities.

- 30% for Wants: such as dining out, hobbies, and entertainment.

- 20% for Savings: focused on debt payments and long-term investments.

📊 It is absolutely essential to track every dollar using modern apps or a simple ledger to visualize your spending patterns. Once you see the hard data, you can make intentional choices rather than impulsive ones that hurt your wallet. 💡 Remember, a budget isn’t a restrictive cage; it’s actually permission to spend guilt-free on what truly matters to you. Setting up automated transfers to your savings can take the struggle of willpower out of the equation entirely. Small changes, like cutting unused digital subscriptions, add up to significant amounts over a calendar year. Stay consistent with this approach, and you’ll find that true financial freedom starts with this single, foundational step.

### Step 2: Building Your Financial Safety Net

After you’ve got a handle on your budget, the next strategic move is building a rock-solid emergency fund. Think of this as your financial insurance policy against life’s many unexpected and expensive curveballs. 🛡️ Ideally, you want to stash away three to six months’ worth of essential living expenses in a separate, dedicated account. This fund should be kept in a High-Yield Savings Account (HYSA) so it earns interest while remaining easily accessible. Without this vital cushion, a simple car repair or medical bill could force you into high-interest debt cycles. It provides a massive psychological relief knowing you won’t be derailed by a temporary career setback or emergency. Start small if you have to—even hitting a $1,000 milestone is a fantastic first achievement to celebrate. 🚀 Avoid the constant temptation to touch this money for anything other than a verified, true emergency. ✋ As your income grows over time, continue to adjust this fund to match your current lifestyle costs. Having this cash readily available is the ultimate ‘sleep well at night’ strategy for any savvy investor. Being prepared for the worst allows you to focus on the best opportunities when they finally arrive. Your future self will thank you for the discipline you show by prioritizing this safety net today.

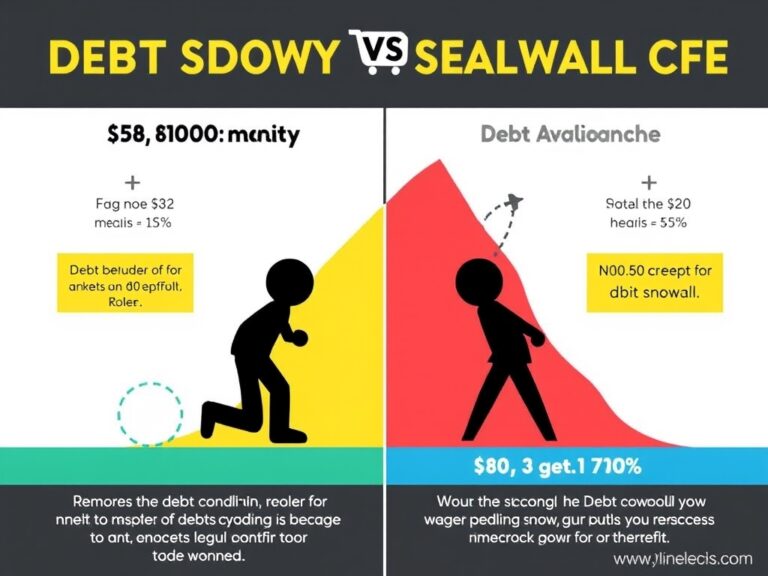

### Step 3: Eliminating High-Interest Debt

Now, let’s talk about the elephant in the room that stops most people: high-interest debt. 🐘 Carrying credit card balances month-to-month is like trying to run a marathon while wearing a heavily weighted vest. To get ahead, you need to prioritize paying off debts with interest rates that exceed 7% or 8%. You might consider using the Debt Avalanche method to pay off the balance with the highest interest rate first. Alternatively, the Debt Snowball method focuses on paying off the smallest balances first to gain psychological momentum. 📉 Every single dollar you save on interest payments is a dollar you can put toward your future wealth. Be extremely wary of ‘Buy Now, Pay Later’ schemes that can clutter your financial life with small, nagging payments. 💳 Consolidating high-interest loans into a lower-rate personal loan can also be a smart move if you have a solid credit score. Remember, not all debt is created equal, but high-interest consumer debt is definitely a primary wealth-killer. Stay disciplined, keep your eye on the long-term prize, and watch your net worth climb as those balances drop. You deserve to live a life free from the stress of mounting monthly interest charges and collection calls. Taking control of your debt is the most immediate way to give yourself a guaranteed return on your money.

### Step 4: Investing for Long-Term Wealth

Once your debt is manageable and your emergency fund is set, it’s finally time to let your money work for you through smart investing. 📈 Investing is the only reliable way to beat inflation and build significant long-term wealth, but it doesn’t have to be overly complicated. Start by embracing diversification through low-cost index funds or ETFs that track the entire stock market. This approach spreads your risk across hundreds of different companies, so you’re never gambling your future on a single stock. 🏢 Focus on time in the market rather than trying to time the market peaks and valleys, which is a losing game. Use strategies like Dollar Cost Averaging to invest a fixed amount regularly, regardless of what the market is doing. 🕒 This removes the heavy emotional stress of watching daily price swings and builds a permanent habit of consistency. Understand your personal risk tolerance; if market drops make you lose sleep, you might need a more balanced portfolio. ⚖️ Keep your investment fees as low as possible, as high management fees can eat away a massive portion of your gains. By starting early and staying invested, you harness the power of compounding to transform small contributions into a fortune. Patience is your greatest ally when it comes to growing a portfolio that can support your lifestyle for years.

### Step 5: Planning for Your Future and Retirement

Finally, let’s look at the big picture: planning for your future self and your ultimate retirement goals. 🌅 Utilizing tax-advantaged accounts like a 401(k) or a Roth IRA is one of the smartest moves any individual can make. If your employer offers a 401(k) match, you should contribute at least enough to get the full amount—it’s essentially free money for your future. 💸 Roth IRAs are particularly incredible because your investments grow tax-free, and you won’t owe the IRS anything when you withdraw later. 🏦 Make it a habit to regularly review your portfolio to ensure your asset allocation still aligns with your retirement timeline. As you get closer to your target retirement date, you might shift toward more conservative investments like bonds. 📉 Don’t forget to account for the impact of inflation, as the purchasing power of a dollar will change significantly over decades. Education is your greatest asset, so keep learning about tax laws and new investment vehicles as they continue to evolve. 📚 By taking these deliberate steps today, you’re not just saving currency; you’re buying your future freedom and total personal security. Financial success isn’t about how much you make, but how much you keep and how hard that money works for you. Start treating your future self like someone you truly care about by making these important decisions today. You have the power to change your financial trajectory, so take that first step toward a prosperous future right now.