Practical Financial Advice: Smart Investing & Money Management Tips

💰 Mastering Your Money Mindset and The Power of Budgeting

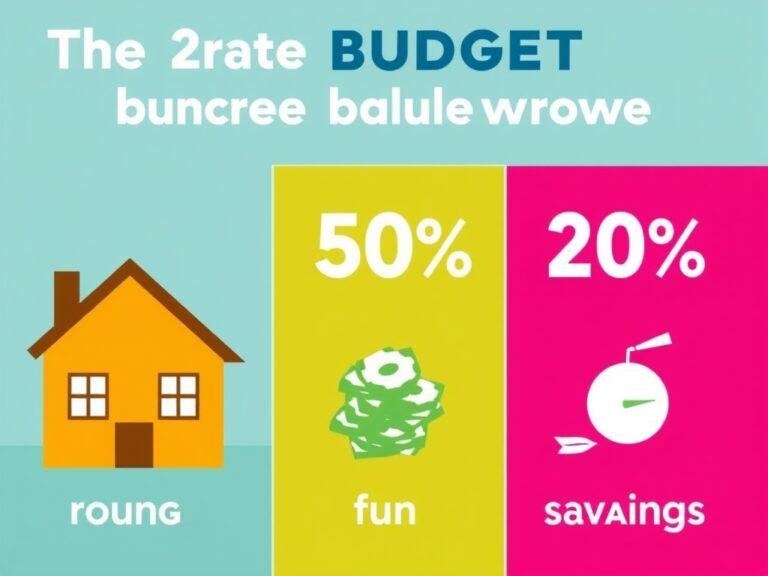

Starting your journey toward financial freedom isn’t just about numbers; it’s about developing a healthy money mindset that prioritizes long-term security over short-term gratification. To truly master your finances, you first need to understand exactly where every dollar is going by implementing a detailed budgeting system. Whether you prefer the 50/30/20 rule or zero-based budgeting, the goal is to ensure your spending aligns with your values and future goals. Tracking your cash flow helps you see how small daily habits translate into large yearly expenses.

- The 50% Rule: Essentials like housing and groceries.

- The 30% Rule: Personal wants and lifestyle choices.

- The 20% Rule: Savings and debt repayment.

By tracking your expenses consistently, you can identify “money leaks” that drain your bank account without you even noticing. Remember, a budget isn’t a cage; it’s a blueprint for your freedom. You should treat your savings as a non-negotiable monthly expense, paying yourself first before you pay any other bills. This proactive approach helps you build a cushion that reduces stress when life throws a curveball your way. Small, intentional changes in your daily habits can lead to massive financial shifts over the course of a year. If you can control your cash flow today, you’re already ahead of the vast majority of people who live paycheck to paycheck. Let’s commit to being the architect of our own financial destiny starting right now! Consistency is the secret sauce that turns a simple plan into a wealth-building machine. You have the power to change your financial trajectory starting today.

🛡️ Building Your Financial Safety Net and Crushing Debt

Before you even think about the stock market, you must focus on protecting your downside by establishing an emergency fund and aggressively tackling high-interest debt. High-interest debt, like credit card balances, acts as a “reverse investment” that compounds against you, so eliminating it is a primary money management tip. Most experts recommend saving three to six months of living expenses in a high-yield savings account (HYSA) to act as your financial shield. This liquidity provides the peace of mind needed to make rational investment decisions later.

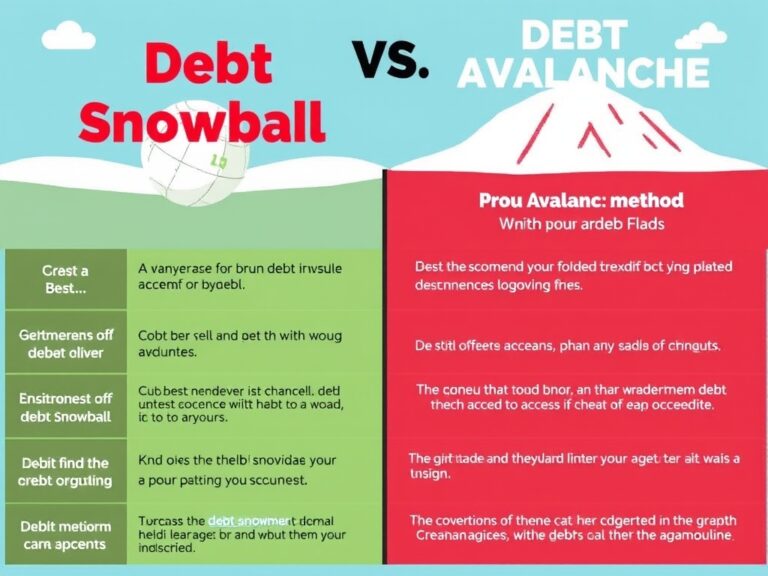

- Debt Snowball: Paying off the smallest debts first for psychological wins.

- Debt Avalanche: Paying off the highest interest rates first to save money.

Compound interest is a double-edged sword; it can either build your wealth or destroy it depending on which side of the debt line you stand. Once your high-interest debt is gone, you can redirect those monthly payments into wealth-building vehicles that grow over time. It’s vital to distinguish between “good debt,” like a reasonable mortgage, and “bad debt” that depreciates in value while costing you a fortune. Having a solid cash reserve prevents you from going back into debt when your car breaks down or an unexpected medical bill arrives. Financial peace of mind comes from knowing you are prepared for the unexpected. Discipline in this stage is what separates those who build wealth from those who stay stuck in a cycle of debt. Focus on the long-term vision of being debt-free and let that motivate your daily financial choices. Success here creates the foundation for every investment decision you will make in the future. You are building a fortress that will protect your family for years to come.

📈 Smart Investing: Making Your Money Work for You

Investing can seem intimidating, but the most effective smart investing strategy is actually quite simple: diversify your assets and stay consistent over the long haul. Instead of trying to pick the next “moonshot” stock, consider low-cost index funds or ETFs that track the entire market and offer instant diversification. This approach lowers your risk while allowing you to capture the growth of the global economy.

- Diversification: Spreading risk across stocks, bonds, and real estate.

- Consistency: Using dollar-cost averaging to buy regardless of market price.

By investing regularly, you benefit from the power of compound interest, which Albert Einstein famously called the eighth wonder of the world. It’s not about timing the market, but rather time in the market that determines your ultimate success as an investor. You should always aim to minimize fees, as even a 1% management fee can eat away hundreds of thousands of dollars over a thirty-year career. Asset allocation should be based on your age and risk tolerance; generally, younger investors can afford to be more aggressive with equities. As you get older, you might shift some of your portfolio into more stable assets like bonds or high-dividend stocks. Don’t let market volatility scare you into selling low; stay focused on your twenty-year goals rather than daily headlines. Smart investing is a marathon, not a sprint, and patience is your most valuable asset in this journey. Every dollar you invest today is a seed that will grow into a tree of financial independence tomorrow. Wealth is built by those who can wait for their investments to mature.

🚀 Retirement Strategy and the Long Game

Your future self will thank you for taking advantage of tax-advantaged retirement accounts like a 401(k) or an Individual Retirement Account (IRA) as early as possible. If your employer offers a 401(k) match, that is essentially a 100% return on your money—never leave that “free money” on the table! These accounts are designed to encourage long-term saving by providing significant tax breaks.

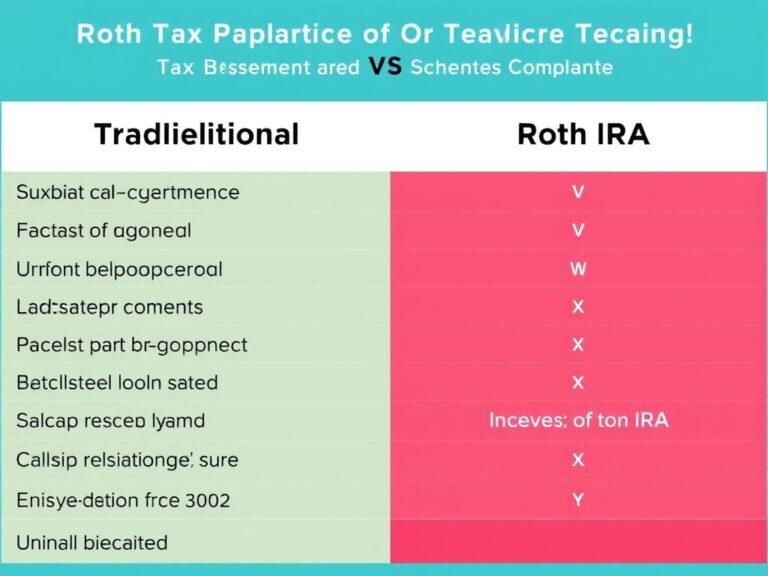

- Traditional IRA/401(k): Tax-deductible contributions now, taxed upon withdrawal.

- Roth IRA/401(k): After-tax contributions now, tax-free withdrawals in retirement.

Choosing between traditional and Roth depends on whether you think your tax bracket will be higher or lower in the future, but having a mix of both is a pro money management move. Automating your retirement contributions ensures that you never forget to invest and helps you avoid the temptation to spend that money elsewhere. The best time to start was ten years ago; the second best time is today. Even if you can only contribute a small amount, the habit of saving for retirement is more important than the initial dollar figure. As your income increases over time, try to increase your contribution percentage to avoid lifestyle inflation from eating your raises. Keep a close eye on your portfolio rebalancing to ensure your risk level stays aligned with your retirement timeline. Managing your taxes through strategic account placement is an expert-level way to keep more of your hard-earned wealth. Remember, retirement isn’t an age; it’s a financial number that you are working toward every single month. Stay disciplined, keep your eye on the prize, and let the system work for you while you focus on living your life. Your golden years deserve a golden foundation.

🔍 Staying the Course: Financial Habits for Life

Finalizing your financial strategy requires a commitment to lifelong learning and the ability to ignore the “noise” of get-rich-quick schemes that saturate the internet. Real wealth is built through boring, repetitive habits like tracking your net worth, reviewing your insurance coverage, and keeping your investment costs low. Consistency in these small actions creates a massive cumulative effect over the decades.

- Net Worth Tracking: Assets minus liabilities to see your overall progress.

- Annual Reviews: Checking in on your goals once a year to make adjustments.

You don’t need to be a Wall Street genius to achieve financial independence; you just need more discipline than the average person. Avoid the trap of lifestyle creep, where your expenses rise just as fast as your salary, preventing you from ever actually getting ahead. Your wealth is what you keep, not what you spend. If you find yourself overwhelmed, don’t hesitate to consult a fee-only fiduciary financial advisor who can provide an objective perspective on your situation. They can help with advanced topics like tax-loss harvesting and estate planning to ensure your legacy is protected for the next generation. Always stay curious and continue reading books or listening to podcasts that reinforce your positive financial habits. The journey to wealth is rarely a straight line, but as long as your trend is upward, you are doing exactly what you need to do. Celebrate your milestones, whether it’s paying off a credit card or hitting your first $10k in investments, to stay motivated. You have all the tools you need to build a prosperous future; now it’s time to go out there and execute the plan! Your financial journey is uniquely yours, so embrace the process and enjoy the growth.