Master Your Finances: Practical Advice and Smart Investing Strategies for Wealth Management

Getting Started: The Foundation of Financial Literacy

Hey there! Have you ever felt like your money is controlling you, rather than the other way around? Mastering your finances is more than just a dream; it’s a journey that starts with a single, intentional step toward financial literacy. When we talk about wealth management, it’s not just for the millionaires next door—it’s for anyone who wants to ensure their hard-earned cash works as hard as they do. To get started, you need to understand your current cash flow and identify where every dollar is heading each month.

- Step 1: Track your spending religiously.

- Step 2: Define your short-term and long-term goals.

- Step 3: Create a realistic budget that leaves room for joy.

Defining your goals gives your money a specific purpose and direction. Creating a realistic budget that leaves room for joy is crucial for long-term sustainability. By setting these foundations, you are essentially building a roadmap for your future self. It’s about creating a lifestyle that prioritizes security and freedom over temporary impulses. Remember, the goal isn’t just to save money, but to create a life where you have the flexibility to make choices without financial stress. 💰 This initial phase is often the hardest because it requires a shift in mindset, but I promise you, the clarity you gain is worth every bit of effort. Let’s dive deep into how you can turn your financial aspirations into a concrete reality starting today.

Building Security: Emergency Funds and Debt Repayment

Once you have a handle on your spending, the next critical phase in your wealth management strategy is building a safety net and tackling high-interest debt. Think of an emergency fund as your financial ‘peace of mind’ bucket, ideally covering three to six months of expenses. Without this cushion, one unexpected car repair or medical bill can send you spiraling back into debt, undoing months of progress. Speaking of debt, it’s important to distinguish between ‘good debt’ like a manageable mortgage and ‘bad debt’ like high-interest credit cards. 💳 Prioritizing debt repayment using the snowball or avalanche method can save you thousands in interest over time.

- The Snowball Method: Paying off the smallest balance first for psychological wins.

- The Avalanche Method: Paying off the highest interest rate first for mathematical efficiency.

While you’re paying off debt, don’t forget to keep your emergency fund growing simultaneously, even if it’s just a small amount. This dual approach ensures that you are both digging yourself out of a hole and building a floor to stand on. It takes discipline, but seeing those balances drop is incredibly motivating for anyone on a wealth-building path. You’ll find that as your debt decreases, your ability to invest and grow your wealth increases exponentially. It’s all about creating a solid foundation so that your future investments aren’t built on shaky ground. Taking these steps early on prevents the common trap of living paycheck to paycheck indefinitely. Secure your foundation now so you can focus on growth later.

Growth Strategies: Smart Investing for the Long Term

Now, let’s talk about the exciting part: smart investing strategies that actually move the needle for your net worth. Investing isn’t about timing the market; it’s about time in the market, allowing the magic of compound interest to do the heavy lifting for you. Whether you’re looking at stocks, bonds, or real estate, the key is diversification to mitigate risk and capture growth across different sectors. 📈 Start by maximizing your employer-sponsored retirement accounts, especially if they offer a match—that’s essentially free money! From there, consider low-cost index funds or ETFs which provide broad market exposure without the high fees of actively managed funds. Your asset allocation should reflect your age, risk tolerance, and when you plan to need the money. Equities provide higher potential for long-term growth but come with more volatility. Fixed Income assets like bonds provide stability and regular interest payments to balance your portfolio. Real Estate offers tangible assets and potential rental income that can serve as a hedge against inflation.

- Equities: Stocks and ETFs for long-term growth.

- Fixed Income: Bonds for portfolio stability.

- Real Estate: Diversification and passive income.

It’s easy to get distracted by ‘meme stocks’ or the latest crypto trends, but a disciplined, long-term approach is what truly builds generational wealth. Stay the course, keep your fees low, and reinvest your dividends to see your portfolio flourish over time. Remember, the best time to start investing was yesterday; the second best time is right now. Don’t let fear of a market downturn keep you on the sidelines. Consistency in your investment contributions is the secret sauce to long-term success.

Advanced Wealth Management: Tax Efficiency and Protection

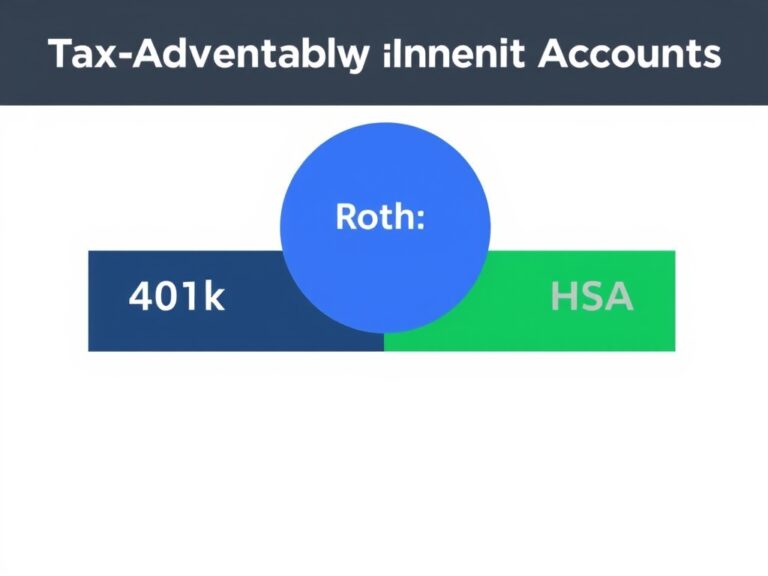

As your portfolio grows, your focus should shift toward advanced wealth management and optimizing for tax efficiency. It’s not just about how much you earn, but how much you actually keep after taxes take their cut. Utilizing tax-advantaged accounts like a Roth IRA or a Health Savings Account (HSA) can significantly boost your long-term returns. 🛡️ Furthermore, regular portfolio rebalancing is essential to ensure your risk level doesn’t drift too far from your original plan as certain assets outperform others. Tax-Loss Harvesting is a great strategy for offsetting capital gains with losses to lower your tax bill. Estate Planning ensures your assets are protected and distributed according to your wishes in the future. Proper Insurance is also a critical component, protecting your wealth against unforeseen catastrophic events that could drain your accounts.

- Tax-Advantaged: Utilizing 401k, IRA, and HSA accounts.

- Rebalancing: Maintaining your target risk level annually.

- Protection: Securing life, disability, and umbrella insurance.

These might sound like complex topics, but they are the pillars that sustain wealth across several decades. Engaging with a fee-only financial advisor can sometimes provide that extra layer of expertise to navigate these nuances effectively. You should also be mindful of inflation, as it silently erodes the purchasing power of any cash sitting idly in a low-interest savings account. By being proactive and strategic, you transition from someone who just ‘has money’ to someone who ‘manages wealth’ with intent. This level of planning provides the ultimate security for your family and your future retirement goals.

Sustainable Success: Discipline and Continuous Learning

Finally, the most underrated aspect of mastering your finances is behavioral discipline and the commitment to lifelong learning. The markets will fluctuate, and economic headlines will often scream for your attention, but the most successful investors are those who can remain calm during volatility. 🧘 Your financial plan should be a living document that you review at least once a year or whenever a major life event occurs. Avoid the trap of lifestyle inflation, where your spending rises exactly in tandem with your raises; instead, aim to ‘save the difference.’ Automate your savings so you never even see the money before it hits your investment accounts. Stay curious and read books or listen to podcasts on personal finance to keep your knowledge sharp.

- Automation: Always pay yourself first.

- Education: Keep learning new financial strategies.

- Patience: Remember wealth building takes time.

Celebrate your milestones, whether it’s hitting a net worth goal or paying off a major loan. Wealth management is a marathon, not a sprint, and your biggest asset is your own consistency and patience over time. By staying informed and sticking to the strategies we’ve discussed, you are setting yourself up for a life of abundance and options. It’s okay to start small, as long as you start with a clear vision of the life you want to lead. Thank you for taking this step today to invest in your knowledge and your future financial well-being. You have the tools, the strategies, and the mindset—now it’s time to go out there and build that wealth!