Master Your Money: Practical Financial Advice, Smart Investing & Management Tips

🌱 Taking Control of Your Financial Future

Hey there! If you’ve ever felt like your bank account is a leaky bucket, you’re definitely not alone, but today is the day we start plugging those holes and building a real foundation for wealth. Mastering your money isn’t just about spreadsheets and complex math; it’s mostly about developing a success-oriented mindset and making conscious choices every single day. When we talk about financial management, we’re really talking about freedom—the freedom to choose your career, your lifestyle, and your future without the constant weight of “how will I pay for this?” hanging over your head. In this guide, we are going to dive deep into smart investing strategies and practical management tips that actually work for regular people, not just Wall Street experts. You need to understand that 💰 wealth is a marathon, not a sprint, and every small step you take today adds up significantly over the next few decades. We’ll explore how to navigate the complexities of the modern economy while keeping your personal goals front and center. By the end of this post, you’ll have a clear roadmap to transition from surviving paycheck to paycheck to thriving with a robust financial portfolio. Let’s get started by looking at how you can transform your daily habits into a powerful engine for long-term prosperity and security. Start by tracking every penny for thirty days to see where your money really goes. This simple act of awareness can be the catalyst for a total financial transformation. Remember, the best time to start was ten years ago, but the second best time is right now.

📊 The Art of Budgeting without the Boredom

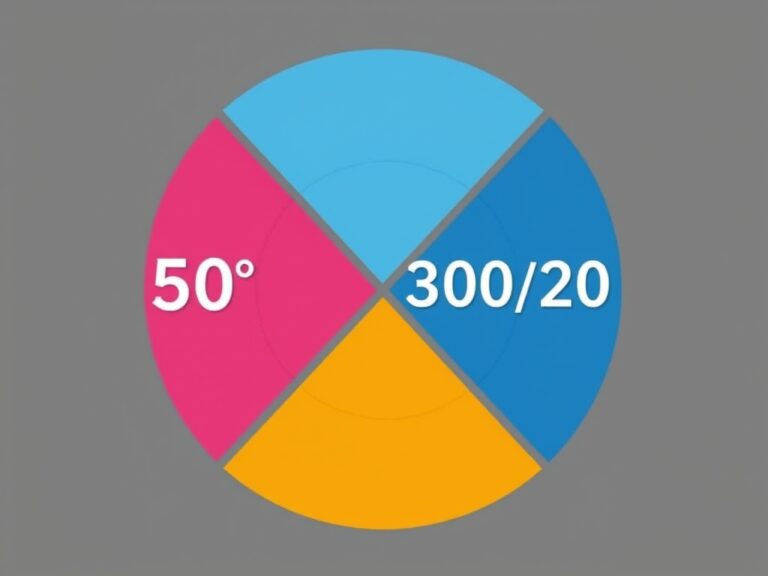

Many people cringe at the word “budget,” but I want you to start thinking of it as a spending plan for your dreams rather than a restrictive set of rules. A solid budget is the cornerstone of money management because it gives every dollar a specific job to do before it even leaves your pocket. One of the most effective methods I recommend is the 50/30/20 rule, which simplifies your finances into three clear categories:

- 50% for Needs: Rent, groceries, utilities, and insurance.

- 30% for Wants: Dining out, hobbies, and that Netflix subscription you love.

- 20% for Savings & Debt: Building your emergency fund and paying down those pesky loans.

By categorizing your income this way, you ensure that your essential costs are covered while still leaving room for 💎 lifestyle enjoyment and future security. It is vital to use digital tools or apps to track your transactions in real-time so you aren’t surprised by your balance at the end of the month. 📉 Tracking your spending reveals patterns you might not even notice, like that daily $6 latte that adds up to nearly $2,200 a year! Once you see the data, you can make informed decisions about where to cut back without feeling deprived. Building an emergency fund of three to six months of expenses is your ultimate safety net against life’s unexpected curveballs. This fund prevents you from dipping into your investments or using high-interest credit cards when the car breaks down. Having this cushion allows you to sleep better at night knowing you are prepared for anything.

🛡️ Crushing Debt and Boosting Your Credit Score

Debt can feel like a heavy anchor dragging behind your financial ship, but with the right strategy, you can cut the line and sail much faster toward your goals. To master your money, you must prioritize high-interest debt, such as credit card balances, which often carry interest rates that eat away at your net worth. There are two popular methods to handle this: the Debt Snowball (paying smallest balances first for psychological wins) and the Debt Avalanche (paying highest interest rates first to save money). 💳 I personally suggest the Avalanche method for those who are numbers-driven, as it mathematically minimizes the amount of interest you pay over time. Beyond just paying it off, you need to understand how your credit score impacts your overall financial health and ability to secure low-rate loans in the future. A high score is a powerful tool that can save you tens of thousands of dollars on a mortgage or car loan.

- Keep utilization low: Try to use less than 30% of your available credit limit.

- Never miss a payment: Automation is your best friend here to ensure 100% on-time history.

- Check your report: Look for errors annually to ensure your record is accurate.

Managing your debt effectively isn’t just about getting to zero; it’s about optimizing your financial reputation so the banking system works for you instead of against you. Once your high-interest debt is gone, that monthly payment can be redirected immediately into your smart investing accounts. Stay disciplined, and remember that every dollar not spent on interest is a dollar that can work for your future self. You are the architect of your financial house, and debt-free living is a very solid foundation.

📈 Smart Investing for Long-Term Wealth Generation

Now that we’ve handled the basics of management, let’s talk about the real engine of wealth: Smart Investing. You don’t need to be a day trader or have a finance degree to grow your money; in fact, the most successful investors often use simple, consistent strategies. The magic ingredient here is Compound Interest, which Albert Einstein famously called the eighth wonder of the world. By reinvesting your earnings, your money starts making money, and then that new money makes even more money in a beautiful upward cycle. 📈 Diversification is your primary defense against market volatility, meaning you shouldn’t put all your eggs in one basket. Instead, consider a mix of assets:

- Index Funds & ETFs: Low-cost ways to own a piece of hundreds of companies at once.

- Real Estate: A tangible asset that can provide both rental income and appreciation.

- Retirement Accounts: Utilizing 401(k)s or IRAs for significant tax advantages.

It’s crucial to start as early as possible because time in the market is significantly more important than timing the market. Don’t let fear of a “crash” keep you on the sidelines; historical data shows that markets trend upward over long periods despite short-term dips. Setting up automatic contributions ensures that you are paying your future self first, regardless of what’s happening in the news cycle. Focus on low-fee investments to keep more of your returns in your own pocket rather than giving them to fund managers. By staying the course and ignoring the noise, you’ll watch your small monthly contributions blossom into a substantial nest egg over the years.

🔐 Tax Efficiency and Protecting Your Hard-Earned Assets

The final piece of the “Master Your Money” puzzle is ensuring that you keep as much of your earnings as possible through tax-efficient planning and protection. It’s not just about what you make, but what you keep after Uncle Sam takes his cut, which is why understanding tax-advantaged accounts is vital. For example, contributing to a Roth IRA allows your money to grow tax-free and be withdrawn tax-free in retirement, which is an incredible advantage. 🛡️ Furthermore, you must protect your assets with the right insurance coverage to prevent a single accident or illness from wiping out years of hard work. This includes health, life, disability, and even umbrella insurance depending on your specific net worth and risk profile. Regularly reviewing your financial plan is also essential because your needs change as you move through different life stages.

- Rebalance your portfolio: Ensure your asset allocation matches your risk tolerance once a year.

- Update beneficiaries: Make sure your legal documents reflect your current wishes.

- Stay educated: Keep reading and learning to adapt to new tax laws and opportunities.

Think of your financial journey as a garden that requires consistent weeding, watering, and protection from pests to truly flourish. By combining disciplined management with strategic growth and proper protection, you aren’t just saving money—you’re building a legacy. You have the power to change your financial trajectory starting today, so take that first step with confidence. Your future self will thank you for the practical financial advice and smart investing steps you put into action right now.