Practical Financial Advice: Smart Investing & Money Management Tips

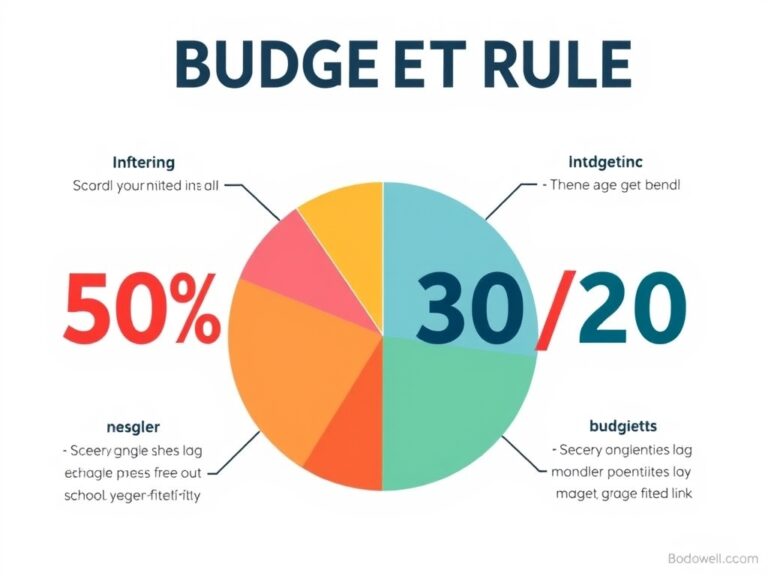

Hey there! Have you ever felt like your money just disappears into thin air the moment your paycheck hits your account? It is a common struggle, but mastering money management is truly the first step toward financial freedom. To get started, you need a clear roadmap of where every dollar goes, which is why creating a comprehensive budget is non-negotiable. One of the most effective methods I recommend is the 50/30/20 rule, which helps simplify your spending habits. Under this framework, 50% of your income goes to needs, 30% to wants, and 20% to savings or debt repayment. You might find that tracking your expenses for a month reveals surprising patterns in your “wants” category.

- You can use apps like Mint or YNAB to automate your tracking process.

- Be sure to review your monthly subscriptions and cancel anything you no longer use.

- Always prioritize your basic ‘needs’ to ensure your survival is covered before spending elsewhere.

By giving every dollar a job, you stop wondering where your money went and start telling it where to go. This shift in mindset from passive spender to active manager is a total game-changer for your bank account. Remember, a budget isn’t a restriction; it’s a tool that grants you the permission to spend without guilt. Let’s make this the month you finally take control of your financial destiny.

Once your budget is in place, the next crucial pillar of smart investing is building a robust safety net known as an emergency fund. Life is inherently unpredictable, and having a dedicated cash reserve can prevent a minor car repair from turning into a major financial crisis. Most experts suggest aiming for three to six months of essential living expenses, but even starting with a small goal of $1,000 can provide significant peace of mind. Where you keep this money matters just as much as how much you save, so look for a High-Yield Savings Account (HYSA). These accounts offer much better interest rates than traditional savings accounts, allowing your money to grow slightly while remaining liquid.

- You should automate your transfers so you “pay yourself first” every month without thinking.

- Keep this account separate from your daily spending account to avoid any impulsive temptation.

- Only touch these funds for true emergencies, not for spontaneous shopping trips or vacations.

Building this cushion is the foundation of a stress-free financial life, as it acts as your personal insurance policy. When you know you’re protected, you can approach riskier investment opportunities with a much clearer head. Think of your emergency fund as the fuel for your future financial engine. Consistency is key, so don’t be discouraged if it takes some time to reach your target. Having this fund allows you to handle life’s curveballs without going into high-interest debt.

Now that you’ve secured your foundation, it’s time to dive into the world of investing to grow your long-term wealth. Many people are intimidated by the stock market, but you don’t need to be a Wall Street pro to see incredible results over time. The “secret sauce” is compound interest, which Albert Einstein famously called the eighth wonder of the world. By investing early and often, your money earns returns, and then those returns earn their own returns, creating a powerful snowball effect. I highly suggest looking into low-cost index funds or ETFs that provide instant diversification across hundreds of companies.

- Diversification reduces your overall risk by not putting all your eggs in one single basket.

- Implementing dollar-cost averaging helps you stay consistent regardless of volatile market swings.

- Focus entirely on the long term rather than trying to time the market’s daily moves.

Market volatility is normal, so the best thing you can do is stay the course and avoid emotional selling when prices dip. Smart investing is a marathon, not a sprint, and patience is your most valuable asset. Every dollar you invest today is a seed that will grow into a massive tree of financial security decades from now. Start small if you have to, but the most important thing is to simply start today. Remember that time in the market beats timing the market every single time.

Managing debt and planning for retirement are two sides of the same coin when it comes to holistic financial health. High-interest debt, like credit card balances, can be a major anchor that prevents you from moving forward, so it’s vital to have a payoff strategy. You might prefer the debt snowball method, where you pay off the smallest debts first for psychological wins, or the debt avalanche method, focusing on the highest interest rates first.

- You should always contribute enough to your 401(k) to get the full employer match because it is essentially free money.

- You should also consider opening a Roth IRA for tax-free growth and tax-free withdrawals in the future.

- Try to avoid taking out new loans while you are aggressively paying down your old ones.

Retirement might seem far away, but the earlier you contribute, the less you have to save later in life thanks to the time value of money. Balancing debt repayment with retirement contributions is a delicate dance, but it is entirely possible with a bit of discipline. Expert-level insights suggest that keeping your debt-to-income ratio low is crucial for maintaining a high credit score. A good credit score opens doors to better mortgage rates and better financial opportunities down the road. Stay focused on your “why” and keep pushing toward that debt-free horizon. Your future self will thank you for the sacrifices you make today. Taking action today is the best gift you can give your older self.

Finally, let’s talk about the most important aspect of money management: your mindset and long-term habits. You can have the best spreadsheet in the world, but if you don’t address your relationship with money, it’s hard to stay on track. Lifestyle creep is a common trap where your spending increases as your income rises, effectively keeping you in the same financial position. To combat this, try to maintain your current lifestyle even after a raise and redirect the extra income toward your investment goals.

- Educate yourself constantly by reading financial books and listening to expert-led podcasts.

- Set specific and measurable financial goals for the next one, five, and ten years.

- Don’t compare your financial journey to someone else’s highlight reel on social media.

Success in personal finance is 20% head knowledge and 80% behavior, so focus on building small, sustainable habits. Practical financial advice isn’t about deprivation; it’s about making choices that align with your true values and long-term happiness. Surround yourself with people who support your financial growth and aren’t afraid to talk about money openly. Remember that every small win counts, and even if you’ve made mistakes in the past, today is the perfect day to start fresh. You have the power to build the life you’ve always dreamed of through intentional spending and smart planning. Let’s make your financial future brighter than ever before. Thank you for taking this first step toward financial mastery with me.