Smart Money Management: Practical Financial Advice & Investing Strategies

Step 1: Mastering Your Budgeting Basics

Hey there! If you’ve ever felt like your bank account is a leaky bucket, you aren’t alone, but it’s time to flip the script on your personal finance journey. Smart money management starts with a rock-solid foundation, and that begins with understanding where every single dollar goes before you even spend it. I recommend using the 50/30/20 rule as a blueprint: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Creating a budget isn’t about restriction; it’s about giving yourself permission to spend on what truly matters while securing your future. One of the most critical steps you can take today is building an emergency fund that covers at least three to six months of living expenses. This fund acts as your financial shock absorber, protecting you from unexpected car repairs or medical bills without derailing your long-term goals. 🏦 You should also consider using automation to move money into your savings account the moment your paycheck hits. By ‘paying yourself first,’ you ensure that your financial health is a priority rather than an afterthought. Remember, consistency is much more important than the initial amount you save. Start small, stay disciplined, and watch how quickly your confidence grows as you take control. 📈 When you treat your money with respect, it starts working for you instead of against you.

Step 2: Destroying High-Interest Debt

Once your foundation is set, it’s time to tackle the ‘wealth killers’ known as high-interest debt, such as credit card balances. 💳 Using smart money management means recognizing that not all debt is created equal, and prioritizing the ones with the highest interest rates can save you thousands. You might want to explore the Debt Avalanche method, where you pay off the highest interest rate first, or the Debt Snowball method, where you pay the smallest balance first for a psychological win. Both strategies are highly effective, but the key is to stop the cycle of borrowing more than you earn immediately. Improving your credit score is another vital component of your overall financial health, as it dictates the interest rates you’ll get on future loans. Make sure you are making all payments on time and keeping your credit utilization below 30% to maintain a healthy score. 📊 Here are some quick tips for managing debt effectively:

- Negotiate lower interest rates with your credit card providers.

- Consolidate high-interest loans into a single, lower-interest personal loan.

- Avoid ‘Buy Now, Pay Later’ traps that encourage lifestyle inflation.

- Review your credit report annually for errors that could be dragging your score down.

By eliminating debt, you free up cash flow that can be redirected toward wealth-building opportunities. It is about shifting your mindset from being a borrower to becoming an owner of your financial destiny. Don’t let debt dictate your future when you can take charge today.

Step 3: Harnessing the Power of Investing

Now, let’s talk about the most exciting part of financial literacy: investing strategies that allow your money to grow while you sleep. The secret weapon of every successful investor is compound interest, which Albert Einstein famously called the eighth wonder of the world. By reinvesting your earnings, your wealth begins to grow exponentially over time, which is why starting as early as possible is so crucial. 🕒 You don’t need to be a Wall Street expert to get started; in fact, simple index funds or ETFs often outperform actively managed funds over the long term. If your employer offers a 401(k) match, that is essentially ‘free money’ that you should maximize immediately to boost your retirement nest egg. 💰 Consider setting up a Roth IRA as well, which provides tax-free growth and tax-free withdrawals in retirement, offering a massive advantage for long-term wealth. Investing is a marathon, not a sprint, so try to avoid the urge to ‘time the market’ based on daily news headlines. Instead, focus on ‘time in the market,’ which has historically proven to be a much more reliable path to success. 🚀 Educational resources like books and podcasts can help you stay informed, but the most important step is simply to begin. Even a small monthly contribution can transform into a significant fortune over several decades if you stay the course. Don’t wait for the ‘perfect’ moment to invest, because time is your most valuable asset. Your future self will thank you for the courage to start today.

Step 4: Diversifying for Long-Term Security

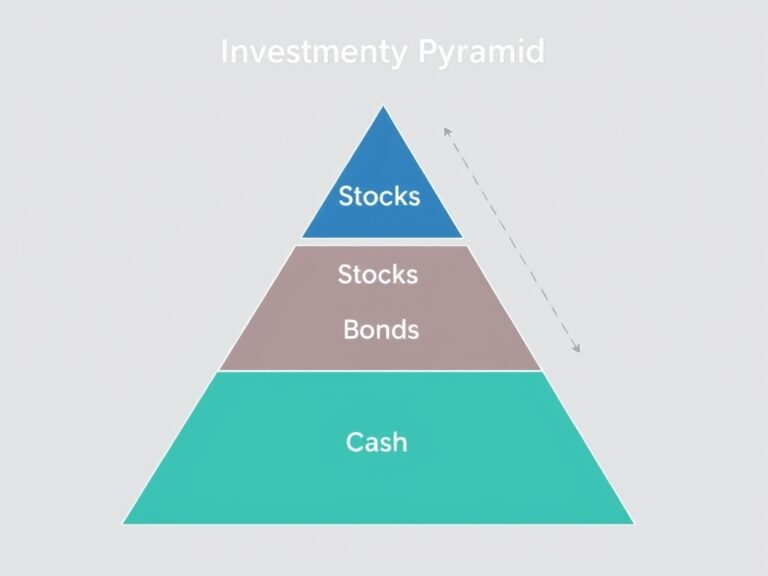

To protect your hard-earned capital, you must understand the principle of diversification, which is the practice of spreading your investments across various asset classes. 🌍 Diversification helps mitigate risk because when one sector of the economy struggles, another may be flourishing, balancing out your overall portfolio performance. A well-rounded strategy typically includes a mix of domestic and international stocks, bonds for stability, and perhaps even real estate or commodities. 🏠 You should also pay close attention to your asset allocation, ensuring it aligns with your age, risk tolerance, and specific financial goals. Here are common asset classes to consider for a balanced portfolio:

- Equities: Stocks that provide growth potential over the long term.

- Fixed Income: Bonds that offer stability and regular interest payments.

- Real Estate: Physical property or REITs that provide passive income.

- Cash Equivalents: High-yield savings accounts for liquidity.

As you get closer to retirement, many experts suggest shifting toward more conservative investments to preserve the wealth you’ve spent years accumulating. However, staying too conservative while you are young can lead to ‘inflation risk,’ where your money loses purchasing power over time. 📉 It’s vital to rebalance your portfolio at least once a year to ensure your original strategy hasn’t drifted. ⚖️ Successful investors remain calm during market volatility, viewing downturns as ‘sales’ rather than reasons to panic and sell. By maintaining a diverse portfolio, you create a resilient financial future. Understanding your risk profile is key to sleeping soundly at night while your money works. Diversification is essentially the only ‘free lunch’ in the world of finance. Make it a core part of your long-term wealth management plan.

Step 5: Planning for a Tax-Efficient Future

Finally, let’s discuss the importance of tax efficiency and long-term planning to ensure you keep as much of your gains as possible. 📑 Using tax-advantaged accounts like HSAs (Health Savings Accounts) can be a brilliant move, as they offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. Additionally, being mindful of capital gains taxes when selling investments in a taxable brokerage account can significantly impact your net returns. 🏦 It’s also wise to automate your investment contributions so that you are practicing dollar-cost averaging, which involves buying more shares when prices are low and fewer when they are high. Beyond the numbers, smart money management involves regular ‘financial check-ups’ where you review your goals and adjust your spending habits as life changes. 🗓️ Whether you’re planning for a house, a child’s education, or an early retirement, having a clear ‘why’ behind your saving will keep you motivated. Surround yourself with positive financial influences and never stop learning about new ways to optimize your wealth. 🧠 Financial freedom isn’t about having a specific amount of money; it’s about having the choices and security that money provides. By following these practical strategies, you are not just managing your money; you are designing a life of abundance and peace of mind. Keep your goals visible and celebrate the small milestones along the way. Financial literacy is a lifelong journey, but the rewards are well worth the effort. You have the power to build the future you’ve always dreamed of.