Smart Money Moves: Practical Financial Advice, Investing, and Management Tips

1. Mastering Your Cash Flow: The Foundation of Financial Freedom

Establishing a solid foundation for your personal finances begins with a deep understanding of your monthly cash flow. Many people view budgeting as a restrictive tool, but in reality, it is a roadmap that grants you the freedom to spend without guilt on things that truly matter. To get started, you should categorize your monthly expenses into fixed and variable costs to identify where your hard-earned money is actually going. A highly effective strategy for beginners and experts alike is the 50/30/20 rule, which helps you balance your lifestyle with your future goals. This rule suggests allocating your income as follows:

- 50% to needs like housing, groceries, and utilities.

- 30% to wants such as dining out, streaming services, or hobbies.

- 20% to savings, investments, and debt repayment.

By automating your savings, you ensure that you are paying yourself first before the temptation to overspend arises at the end of the month. Tracking your net worth monthly can also provide a high-level view of your progress and keep you motivated on your journey. Remember, the goal of a budget is not perfection but consistent discipline in managing your daily transactions. Utilizing modern fintech apps can simplify this process by automatically categorizing your spending habits for easier review and adjustment. 💰 With a clear vision of your finances, you can make informed decisions that align with your long-term aspirations. This proactive discipline transforms your relationship with money from one of constant stress to one of strategic management. Ultimately, mastering your cash flow is the most critical step toward achieving financial independence.

2. Strengthening Your Safety Net and Tackling High-Interest Debt

Once your budget is in place, the next smart money move is to build a robust emergency fund to protect yourself against life’s unexpected curveballs. Financial experts generally recommend saving between three to six months of essential living expenses in a dedicated high-yield savings account. This liquid cushion prevents you from falling back into debt when a medical bill, job loss, or car repair suddenly appears. 🛡️ Speaking of debt, it is crucial to prioritize the elimination of high-interest obligations, such as credit card balances, which can rapidly erode your wealth. You might consider the Debt Avalanche method, where you focus on paying off the account with the highest interest rate first to save money. Alternatively, the Debt Snowball method allows you to pay off smaller balances first for the psychological wins that keep you motivated. Reducing your debt-to-income ratio not only improves your credit score but also frees up more capital for future investments. It is also wise to review your various insurance policies periodically to ensure you are adequately covered without being over-insured. Keeping your financial liabilities low is a cornerstone of building true financial security and long-term peace of mind. Consistency is key here; even small extra payments can significantly reduce the total interest paid over the life of a loan. By securing your financial base, you create a powerful launching pad for more aggressive wealth-building strategies. This safety net allows you to take calculated risks in other areas of your life without fearing total financial ruin.

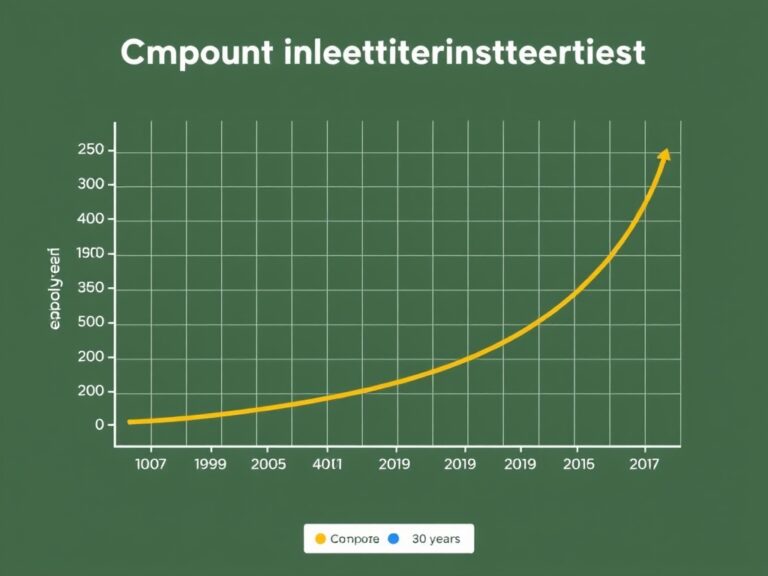

3. Strategic Investing: Harnessing the Power of Compounding

To truly grow your wealth, you must transition from being just a saver to being an investor, allowing your money to generate its own earnings. The stock market is one of the most accessible vehicles for long-term growth, especially when you leverage the incredible power of compound interest. Starting early is often more important than starting with a large sum because time is the greatest multiplier for your investment returns. Portfolio diversification is your best friend in this journey, as it helps mitigate risk by spreading your capital across various sectors. Consider a mix of the following assets to build a balanced portfolio:

- Index Funds: Low-cost options that track the performance of the broader market like the S&P 500.

- Dividend Stocks: Shares in companies that pay you a portion of their profits regularly as passive income.

- Real Estate: Physical properties or REITs that provide rental income and potential appreciation over time.

Avoid the common trap of trying to time the market based on news cycles; instead, practice Dollar-Cost Averaging for better results. 📈 Understanding your unique risk tolerance is vital before picking specific assets to ensure you can stay the course during market volatility. You should aim to keep your investment fees low, as high management costs can eat into your gains significantly over several decades. Investing is fundamentally a marathon, not a sprint, and patience is often rewarded with substantial financial gains for those who wait. A well-diversified portfolio acts as a vital hedge against the failure of any single sector or individual company. Staying educated about market trends and economic shifts will empower you to adjust your strategy as your life circumstances change. By making your money work for you, you create a path toward generational wealth and early retirement options.

4. Planning for the Future: Retirement and Tax Optimization

A comprehensive financial plan is never complete without a strategy for retirement planning and maximizing your tax efficiency. You should start by taking full advantage of employer-sponsored plans like a 401(k), especially if they offer a matching contribution. If you have further capacity, exploring a Roth IRA or a Traditional IRA can provide significant tax advantages depending on your goals. 🏦 Understanding the nuanced difference between tax-deferred and tax-free growth will help you choose the right vehicle for your specific needs. It is also beneficial to look into Health Savings Accounts (HSAs), which offer a unique triple-tax advantage for medical expenses. Rebalancing your portfolio annually ensures that your asset allocation remains aligned with your target retirement date and risk level. As you approach retirement age, your focus may naturally shift from aggressive growth to wealth preservation and steady income generation. Consulting with a certified financial planner can provide personalized insights into complex tax laws and sophisticated estate planning techniques. Ensuring your beneficiaries are updated on all financial accounts is a simple but critical step in protecting your family’s future legacy. By being proactive today, you ensure a comfortable and dignified lifestyle during your golden years without financial worry. Tax-loss harvesting is another advanced technique you can use in taxable accounts to offset gains and reduce your overall tax bill. Ultimately, retirement planning is about buying back your time so you can enjoy your life on your own terms.